Housing Market Oddities and Opportunities?

I thought the big news from this past month would have been the election, but A) We’re all tired of hearing about it, and B) it’s not directly impacting the lives of clients so I have trouble spending too much time on it.

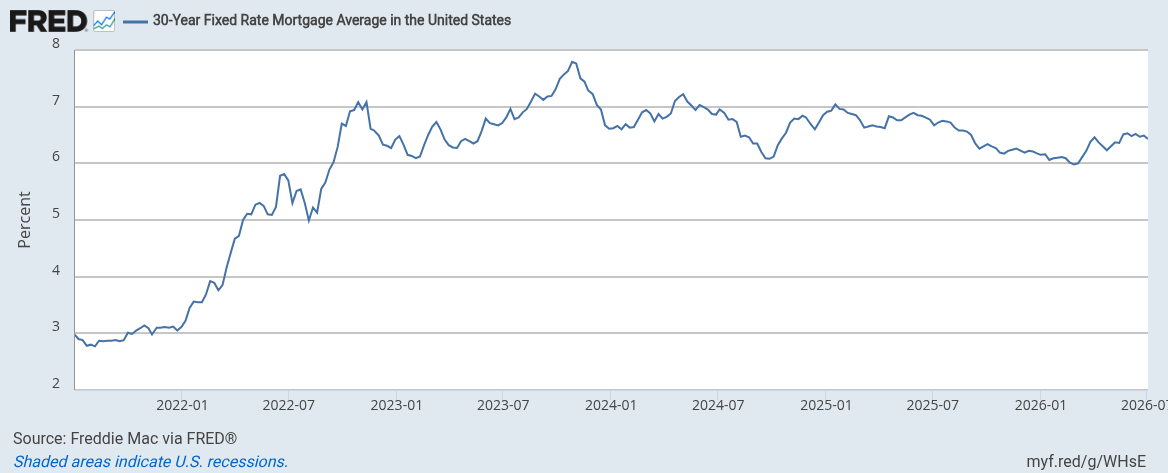

We have a few clients and contacts in the mortgage industry. They went from writing mortgages as fast as they humanly could to nothing, zilch, nada in 6 months. Interest rates are the primary cause. As I write this, the interest rate on a 30-year fixed mortgage is 6.49%. That's following a decline of almost 0.5% in the past month.

You can see that rates moved from 3.22% up to over 7% in 11 months. That is a lot! People are hesitant to build homes or buy new homes; sellers are not as motivated to move because they can not buy as much after selling. What does that mean for home values? If demand for new houses is still high, and supply is still low, you shouldn’t see a pullback in home prices as we saw in 2007-2008. Brian Wesbury from First Trust says, “The bottom line is that what we are seeing right now in the housing

market is a bad case of indigestion from higher interest rates…We project continued gains in rents in the next few years as home prices are roughly unchanged. The maximum drop in home prices from the peak to the bottom in this cycle should be around 5%, not a 25% implosion like last time.”

When I think about opportunities, if you were already looking to move, this may help keep people from buying too much house. We saw it all the time that when interest rates were low, people were buying at the very top of their income range. That’s great until the property tax bill, the furniture bill, and the HVAC, etc. come due. It’s just more costly to operate a bigger house. Look at the increase in the average size of houses since 1975. Almost 1,000 square feet bigger on average!

I saw a tweet from a financial planner that I follow that was interesting. “A married couple with a 30-year, 7.5% fixed-rate mortgage will be able to itemize deductions with only a $375,000 purchase (with a 20% down payment).” With the Tax Cuts and Jobs Act in 2018, Congress limited state and local tax deductions to $10,000 per year and increased the standard deduction from $12,000 to $24,000 for married couples. The higher standard deduction means that very few people were able to itemize

deductions (pre-2018 standard deduction was about 70% of taxpayers, now it's about 90%), which made it harder to itemize charitable giving, large medical expenses, and more.

I could definitely see the doom and gloom angle, but I like to look on the positive side and see the opportunities where possible.

* The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.