The GPS Approach to Retirement: Why Detours Won’t Derail Your Plan

I was listening to the Modern Wisdom podcast recently, and a guest brought up an idea he called "GPS brain." The gist of it was that when you miss a turn, your GPS doesn't berate you. It doesn't ask why you weren't paying attention or tell you that you've ruined the whole trip. It just recalculates and gives you the next direction. Maybe your arrival time slips by five minutes. Then it keeps going.

That stuck with me, because it's exactly how I think about retirement planning.

A lot of people treat retirement like a rigid sequence. Do A, then B, then C, in that order, and if you miss a step, the whole thing falls apart. They assume a missed turn is permanent. In my experience, it rarely is. The famous economist Thomas Sowell once made the point that there are no solutions, only trade-offs, and that's a useful way to look at your finances. An expensive stretch in your late 40s, when your kids are in three sports and a music program, isn't a death sentence for your retirement. The GPS just recalculates your arrival time.

Pick the Destination Before the Number

Here's where I see people get stuck. They start at the end. A big, round number ("I want $2 million") or a target age ("I'll retire at 65"). Neither one means much until you know where you're actually going.

Think about driving south from St. Louis. Destin is about 11.5 hours away. Disney (Orlando) is closer to 14.5. Fort Myers Beach is 16.5, Miami pushes 18, and Key West is around 21. "Florida" isn't a destination. It's a direction. The specifics change everything about how you plan the trip.

Retirement works the same way. The plan isn't really about hitting an arbitrary number. It's about clarifying what your life actually costs and what you want your days to look like. Once we know the real destination, the math gets a lot clearer: how much you'll need from your portfolio, and for how long. Those two variables drive almost everything.

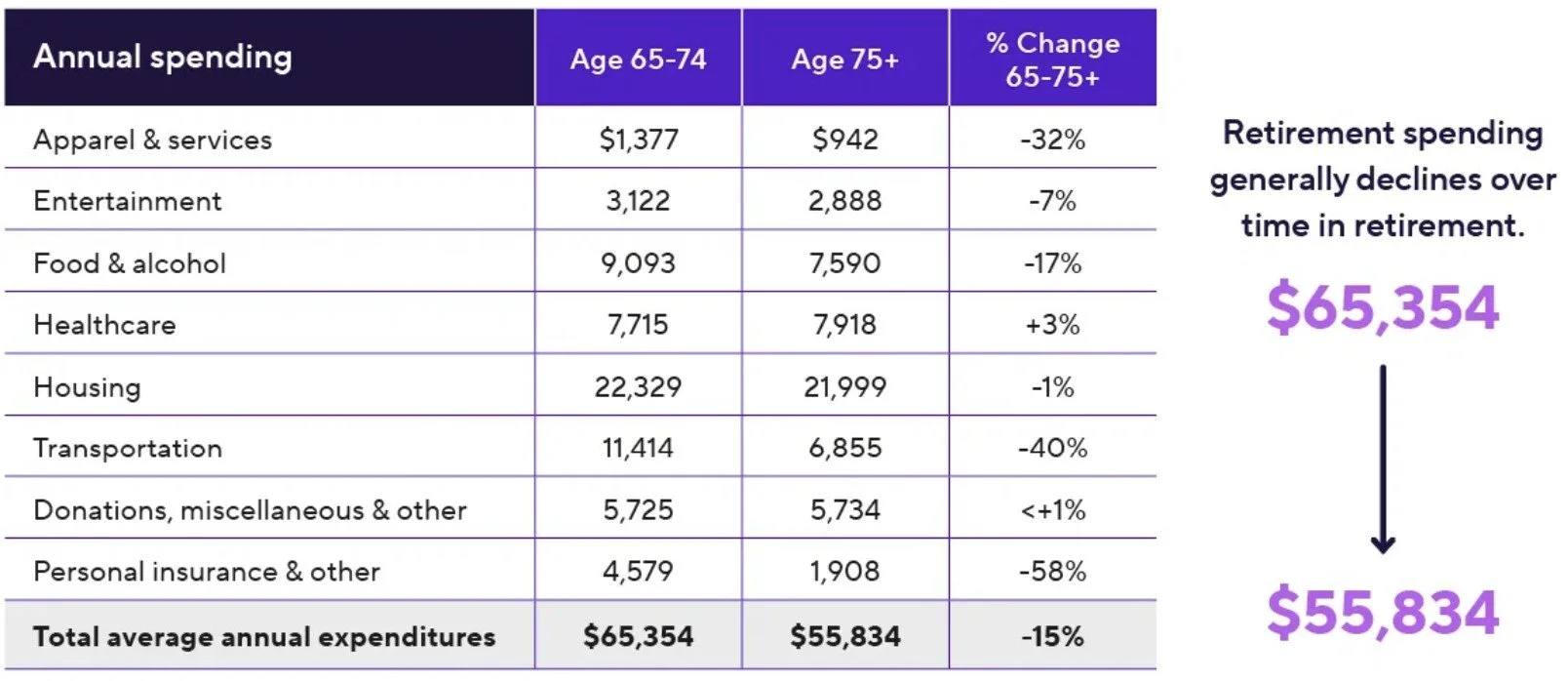

And those expenses don't stay flat across retirement. The first decade or so, what we call the "go-go" years, can be nearly as expensive as your working years. People travel more. They tackle the home projects they'd been putting off and finally do the things their working years didn't leave room for. Spending generally eases as the years go on. Corebridge data shows total annual expenditures drop about 15% from ages 65-74 to 75 and up. In our planning, we typically build in a 20% reduction in normal living expenses to account for that natural decline.

Our Job Is to Be Your GPS

Once you've picked the destination, my job as your planner is to help you navigate. Sometimes that means pointing out that the scenic route is longer. Retiring at 66 instead of 61 is a real trade-off, and you get to decide whether the extra five years of work is worth what it buys you. To keep the analogy going, you don't want to pack for a quiet beach trip and then find yourself standing in line for Space Mountain. The destination you choose should match the trip you actually want.

A lot of people start driving without ever setting up the GPS. They're moving, but they don't realize they've drifted off course until they're hours behind. That's what our annual meetings are designed to catch. We check the route, see whether an alternate path makes sense, and flag when you need to fill the tank because the next station is a long way off.

The Detours Are the Whole Point

What catches people off guard is that the trip will throw detours at you. That's not a sign the plan failed. It's the reason you build the plan in the first place.

A job change is one of the big ones. Maybe you take a new role with a higher salary, but a worse 401(k) match, or you leave to start something of your own, and your income gets lumpy for a few years. Either way, the route changes, and we navigate around it. A market drop right before you'd planned to retire is another. It feels like a road closure with no detour, but historically, markets have moved through these stretches and recovered. A plan built with that possibility in mind has room to absorb it without forcing a panic decision.

Then there are the happier detours. An inheritance lands, or you sell a business, or the kids finish college two years earlier than you budgeted for. Those are turns, too, and they can pull your arrival time forward instead of pushing it back. The point isn't that every surprise is a setback. It's that a good plan flexes in both directions.

What ties all of this together is checking your route regularly and recalculating when the road changes. One conversation at the start of the trip isn't enough, because the conditions keep changing, sometimes a detour, sometimes a faster route that just opened up. Checking in once a year is what lets us catch a drift while it's still small and cheap to correct, rather than discovering it when you're three hours behind and out of options.

The Road Is Going To Change. Plan For It.

Retirement planning isn't about charting one perfect path and following it without deviation. Nobody does that, and the people who expect to are usually the ones who get rattled when life intervenes. The real work is picking a destination you actually want, then staying flexible enough to adjust when the road does something you didn't expect.

That's the mindset I want every client to carry. A missed turn isn't a failure of discipline or a reason to question whether you'll get there. It's information. We take that information, recalculate, and keep driving toward the place you chose. Some years, the arrival time moves up. Some years it moves back. As long as we're checking the map together and the destination is clear, you stay in control of the trip the entire way.

Rob Clark, CFP®, is a CERTIFIED FINANCIAL PLANNER® professional at INT Wealth Planning, serving upper-income professionals in the Greater St. Louis area. Rob specializes in simplifying complex financial decisions and creating tailored strategies for wealth accumulation and retirement planning. INT Wealth Planning focuses on helping clients get organized, make informed financial decisions, plan for retirement, and pursue financial confidence. Rob can be reached at (636) 777-4207, via email at rob@intwealthplanning.com, or online at www.intwealthplanning.com.

This material has been prepared in collaboration with Crystal Marketing Solutions, LLC, and has been edited with the assistance of artificial intelligence tools. The information presented is based on sources believed to be reliable and accurate at the time of publication. This material is for educational purposes only and does not necessarily reflect the views of the author, presenter, or affiliated organizations. It should not be construed as investment, tax, legal, or other professional advice. Always consult a qualified professional regarding your specific situation before making any decisions.